The path to investment success can be bumpy and unpredictable. Market volatility is inevitable and should be embraced as part of the investing experience. But some investors find sudden market swings disturbing and may sell their holdings after a sudden decline. This can dramatically reduce their long-term returns and possibly postpone their financial goals.

Fortunately, there is a strategy that can make it easier to stay invested through periods of market turbulence. A portfolio that focuses on reducing the risk of large losses during downturns can also reduce the time it takes to recover from portfolio declines. This can be critical to generating long-term compounded growth.

For investors who want to be fully invested across market cycles, low-volatility investing can give them more confidence to remain focused on their long-term investment objectives and reduce the temptation of market timing.

The problem with market timing

Market volatility is a major cause of investor anxiety and can prompt investors to abandon their asset allocation plan. Too often, these investors believe they can wait on the sidelines, then jump back into the market in time for the recovery that follows.

The problem with this plan is that the best and worst days in the market usually happen in close succession, often within the same week. Missing the first days of a rally will likely result in underperformance compared to an investor who simply stayed invested. If some of the best days are missed, it will take longer for investors to recover their losses.

Low-volatility strategies have historically performed well in turbulent markets, delivering market-like returns over the long run. This contradicts the idea that higher risk will bring higher returns. Yet it has been demonstrated repeatedly.

Why low volatility investing works

Investors often believe that risky (more volatile) assets will earn them higher returns, so they are willing to pay more for them. This has been dubbed the “lottery effect,” where the remote chance of the large return is more appealing than a smaller gain that is far more likely.

This higher demand can lead to an overvaluation of volatile stocks when markets are rising. However, when the market corrects, this overvaluation can lead to declines that are much larger than the overall market. On the other hand, low-volatility stocks tend to experience much smaller declines because they tend not to be as overvalued to begin with.

To break even from large losses, an investor needs a much larger gain. For example, a 10% loss requires a gain of 11% to break even, but a 40% loss requires a gain of 67%. Because low-volatility stocks tend to have smaller declines, they require shorter recovery periods to recover. This improves the portfolio’s long-term compounded growth – in essence, winning by losing less.

Shorter recovery periods

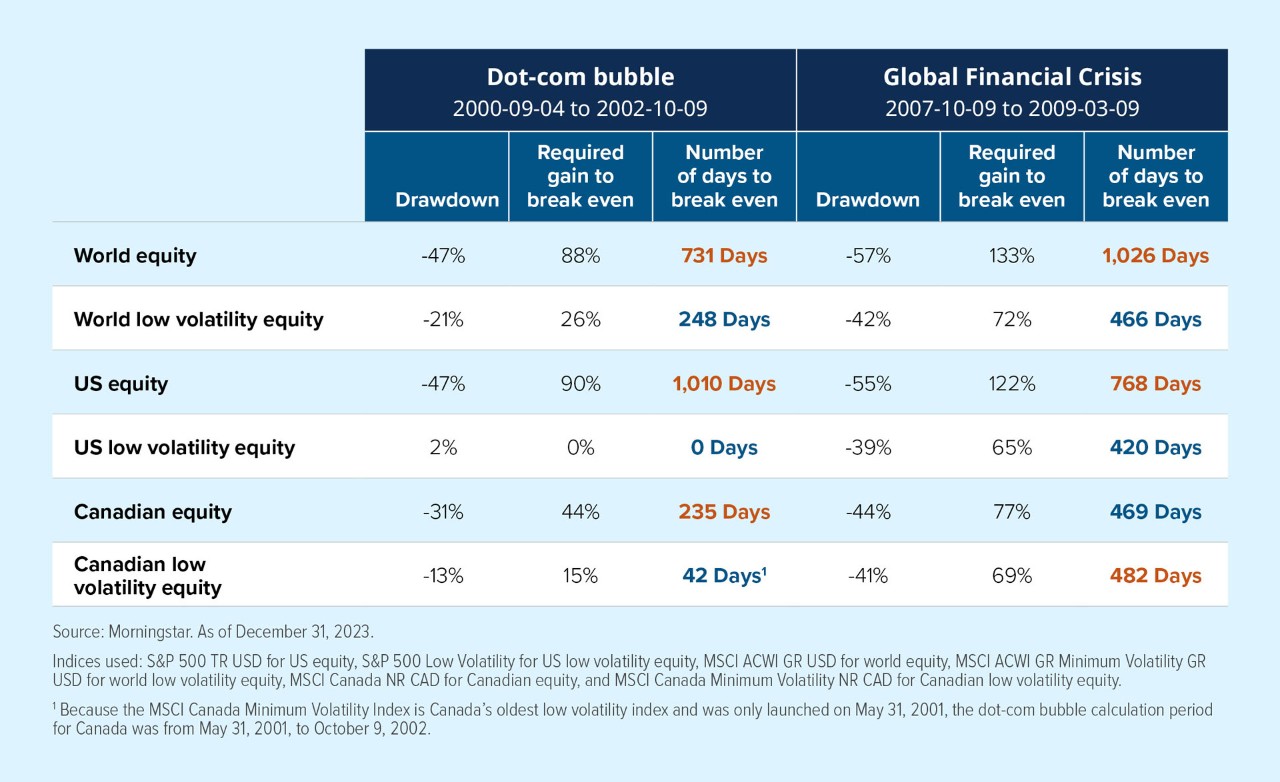

Historically, low volatility strategies have delivered performance similar to the overall market, with far less volatility. This has been demonstrated across various regions. Consider two of the most dramatic market declines since 2000 — the dot-com bubble and the global financial crisis. In both cases, a low volatility strategy preserved capital during market downturns, which helped limit the losses and shorten the recovery period.

During the global financial crisis, world equity declined 57%, a loss that took 1,026 days to recover from the trough. In contrast, world low-volatility equity had a 42% drawdown and took only 466 days to break even.

Buy-and-hold low volatility versus market timing

Market timing strategies are ineffective because predicting the right exit and entry points is nearly impossible. Historically, periods of high volatility include days with the best gains, often immediately following the worst days.

Mistiming exit and entry points can cost investors growth opportunities, eventually leading to significant underperformance.

Mackenzie low-volatility solutions

A low volatility strategy can be an effective core portfolio holding, as it can reduce risk without losing long-term growth and still achieve market-like returns over the long term.

The Mackenzie low-volatility strategies use a flexible, high-conviction set of alpha factors to construct a core, risk-aware portfolio designed with the goal of outperforming in a wider array of market environments.

The strategies are suitable as a core holding for investors who want to add a low-volatility component to their portfolios for a smoother ride across all market cycles or as a complement to portfolios that have a tilt towards a high-volatility or growth style.

The Mackenzie Global Quantitative Equity Team has a strong track record of managing low-volatility strategies across regions, using a data-driven approach that combines robust research and strong risk management to enhance investment decision-making.

Learn more about Mackenzie’s Low Volatility offerings

| C$ Series Fund Codes (Prefix: MFC) | |||

A/SC | F | PW | ||

Fund | FE | BE

| FE | FE |

7537 | 7538 | 7542 | 7545 | |

ETF | Ticker |

| ||

MWLV |

| |||

MULV | ||||

MCLV | ||||

1 The Volatility Effect Revisited: David Blitz, Pim van Vliet and Guido Baltussen, 2019.